All Categories

Featured

Table of Contents

[/video]

Holding money in an IUL dealt with account being attributed passion can typically be much better than holding the cash money on deposit at a bank.: You have actually constantly desired for opening your very own pastry shop. You can borrow from your IUL plan to cover the first expenses of leasing an area, purchasing equipment, and employing personnel.

Personal car loans can be acquired from standard banks and lending institution. Below are some bottom lines to consider. Charge card can give a flexible method to borrow money for really short-term durations. Obtaining money on a credit history card is typically extremely expensive with annual percent rates of interest (APR) typically getting to 20% to 30% or more a year.

The tax obligation therapy of plan finances can vary dramatically depending on your nation of home and the certain regards to your IUL plan. In some areas, such as North America, the United Arab Emirates, and Saudi Arabia, policy car loans are normally tax-free, providing a substantial benefit. In various other jurisdictions, there may be tax obligation ramifications to think about, such as potential tax obligations on the lending.

Term life insurance just offers a death advantage, without any kind of cash money worth build-up. This suggests there's no money worth to borrow versus.

Infinite Insurance And Financial Services

Imagine stepping right into the financial cosmos where you're the master of your domain, crafting your very own course with the finesse of a skilled banker however without the constraints of towering organizations. Welcome to the globe of Infinite Banking, where your financial fate is not simply an opportunity however a concrete reality.

Uncategorized Feb 25, 2025 Cash is one of those points all of us handle, however most of us were never ever really taught how to use it to our advantage. We're told to conserve, spend, and budget, however the system we operate in is made to keep us dependent on banks, constantly paying passion and costs just to accessibility our own money.

She's an expert in Infinite Banking, a method that assists you take back control of your financial resources and develop genuine, long-term riches. It's a real approach that well-off families like the Rockefellers and Rothschilds have been using for generations.

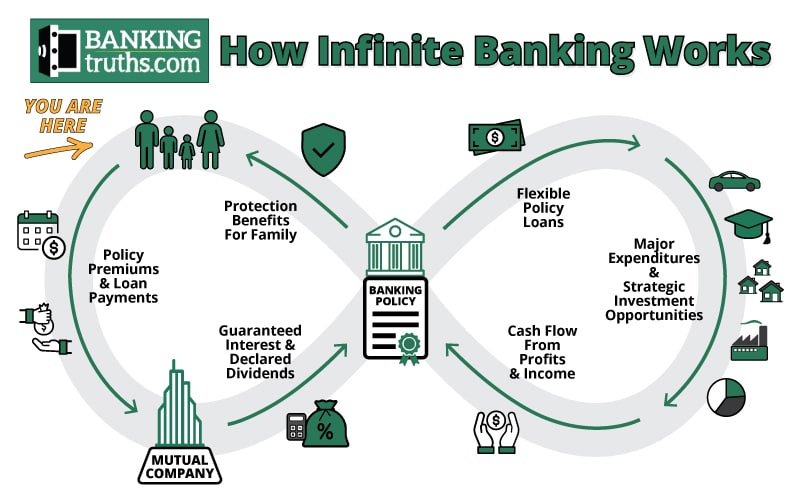

Currently, prior to you roll your eyes and think, Wait, life insurance policy? That's boring.stay with me. This isn't the kind of life insurance policy the majority of people have. This is a high-cash-value plan that enables you to: Shop your money in an area where it grows tax-free Borrow against it whenever you need to make investments or significant acquisitions Earn continuous compound rate of interest on your money, even when you borrow against it Consider just how a financial institution functions.

With Infinite Banking, you become the financial institution, making that rate of interest rather than paying it. It's a total paradigm shift, and when you see exactly how it functions, you can't unsee it. For the majority of us, cash spurts of our hands the second we obtain it. We pay costs, make purchases, pay down debtour dollars are constantly leaving us.

Infinite Banking Concept Wiki

The insurance coverage firm does not require to get "paid back," since it will certainly simply be deducted from what gets distributed to your beneficiaries upon your expiration date, as Hannah so euphemistically called it. You pay on your own back with passion, similar to a financial institution wouldbut now, you're the one profiting. Allow that sink in.

It's concerning rerouting your cash in a manner that constructs wide range rather than draining it. If you're in actual estateor wish to bethis strategy is a found diamond. Allow's state you want to acquire an investment home. Instead of mosting likely to a financial institution for a car loan, you obtain from your own plan for the deposit.

You utilize the car loan to buy your building. Rental income or benefit from the deal pay back your policy rather than a bank. This means you're building equity in your policy AND in property at the same time. That's what Hannah calls double-dippingand it's exactly just how the wealthy keep growing their cash.

Infinite Financial

Right here's the thingthis isn't a financial investment; it's a cost savings technique. Your money is ensured to grow no issue what the stock market is doing. You can still spend in real estate, supplies, or businessesbut you run your money with your plan first, so it maintains growing while you spend.

See to it you function with an Infinite Banking Idea (IBC) specialist who recognizes how to set it up correctly. This method is an overall way of thinking change. We have actually been trained to assume that financial institutions hold the power, yet the reality isyou can take that power back. Hannah's family has actually been using this strategy given that 2008, and they currently have over 38 policies moneying property, investments, and their family's monetary tradition.

Becoming Your Own Lender is a message for a ten-hour program of guideline concerning the power of dividend-paying entire life insurance. The industry has actually concentrated on the death benefit top qualities of the agreement and has actually neglected to properly describe the financing abilities that it provides for the plan proprietors.

This book demonstrates that your requirement for financing, during your life time, is much higher than your requirement for security. Address for this demand with this tool and you will certainly wind up with even more life insurance coverage than the companies will issue on you. A lot of everyone recognizes with the fact that can borrow from an entire life policy, however due to the fact that of how little costs they pay, there is minimal access to cash to fund major things required during a life time.

Actually, all this publication includes in the equation is scale.

{kind=link}

Latest Posts

Byob: How To Be Your Own Bank

Banking Concept

Infinite Banking Calculator