All Categories

Featured

Table of Contents

For the majority of people, the greatest issue with the infinite banking principle is that preliminary hit to early liquidity created by the expenses. Although this con of boundless banking can be decreased substantially with appropriate plan design, the very first years will certainly always be the worst years with any type of Whole Life plan.

That said, there are particular limitless banking life insurance coverage plans made primarily for high early money value (HECV) of over 90% in the first year. Nevertheless, the long-term performance will often significantly delay the best-performing Infinite Banking life insurance policy plans. Having access to that additional four figures in the very first couple of years may come at the expense of 6-figures later on.

You really get some substantial long-lasting benefits that assist you recover these early costs and after that some. We discover that this hindered early liquidity problem with limitless banking is a lot more mental than anything else when thoroughly checked out. As a matter of fact, if they absolutely needed every cent of the money missing out on from their infinite banking life insurance policy in the initial few years.

Tag: unlimited financial idea In this episode, I speak regarding finances with Mary Jo Irmen who shows the Infinite Financial Idea. With the rise of TikTok as an information-sharing system, financial suggestions and methods have located a novel means of spreading. One such method that has actually been making the rounds is the limitless financial idea, or IBC for brief, garnering recommendations from stars like rapper Waka Flocka Fire.

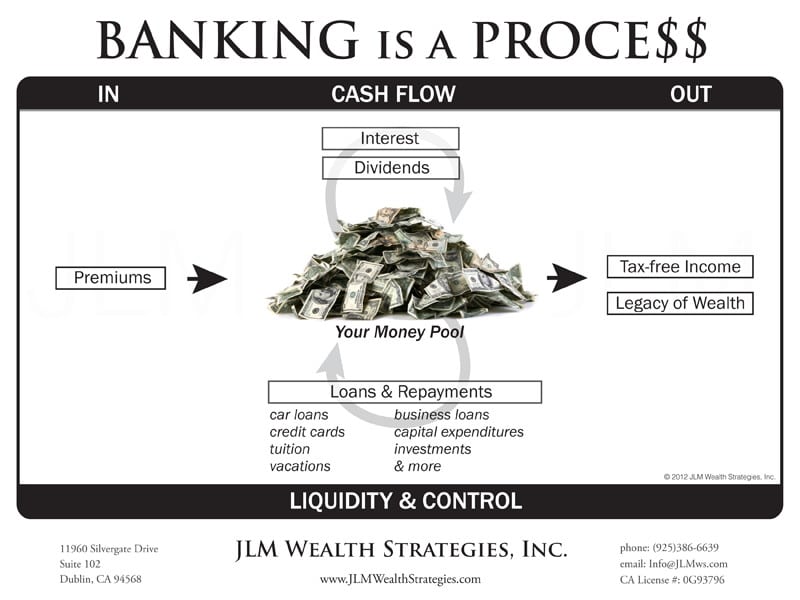

Within these policies, the cash worth grows based upon a price established by the insurance company. When a significant cash money worth collects, policyholders can obtain a cash worth finance. These loans differ from traditional ones, with life insurance policy functioning as security, implying one can lose their coverage if borrowing exceedingly without appropriate money worth to sustain the insurance coverage expenses.

And while the attraction of these plans is apparent, there are natural constraints and risks, requiring thorough cash money value tracking. The approach's authenticity isn't black and white. For high-net-worth people or company owner, specifically those utilizing approaches like company-owned life insurance policy (COLI), the advantages of tax obligation breaks and compound growth could be appealing.

The Infinite Banking System

The attraction of unlimited financial doesn't negate its challenges: Expense: The fundamental need, an irreversible life insurance policy, is costlier than its term counterparts. Eligibility: Not everybody receives whole life insurance policy due to rigorous underwriting processes that can exclude those with certain health and wellness or way of living problems. Complexity and danger: The intricate nature of IBC, coupled with its risks, may hinder several, particularly when less complex and much less risky choices are readily available.

Assigning around 10% of your monthly revenue to the policy is simply not feasible for many people. Utilizing life insurance coverage as an investment and liquidity resource calls for discipline and tracking of plan cash value. Get in touch with a financial advisor to establish if limitless financial lines up with your top priorities. Part of what you read below is simply a reiteration of what has actually currently been stated above.

Prior to you get yourself into a scenario you're not prepared for, know the adhering to initially: Although the principle is generally marketed as such, you're not really taking a financing from yourself. If that held true, you would not need to repay it. Instead, you're borrowing from the insurance policy company and have to repay it with interest.

Some social media posts suggest using cash money worth from entire life insurance policy to pay down charge card debt. The idea is that when you settle the car loan with passion, the quantity will be sent back to your investments. However, that's not how it works. When you pay back the loan, a section of that rate of interest goes to the insurance policy business.

For the first numerous years, you'll be paying off the payment. This makes it very difficult for your plan to build up worth throughout this time. Unless you can manage to pay a few to numerous hundred dollars for the following years or even more, IBC will not function for you.

Infinite Banking Policy

If you need life insurance policy, right here are some useful suggestions to think about: Consider term life insurance coverage. Make sure to shop around for the finest price.

Copyright (c) 2023, Intercom, Inc. () with Booked Font Name "Montserrat". This Typeface Software is accredited under the SIL Open Typeface License, Version 1.1. Copyright (c) 2023, Intercom, Inc. (legal@intercom.io) with Scheduled Font Name "Montserrat". This Typeface Software program is accredited under the SIL Open Up Typeface Certificate, Version 1.1.Avoid to main material

Infinite Banking Course

As a CPA concentrating on property investing, I've combed shoulders with the "Infinite Financial Idea" (IBC) a lot more times than I can count. I have actually also interviewed professionals on the subject. The major draw, aside from the noticeable life insurance policy benefits, was constantly the idea of building up cash value within a permanent life insurance policy policy and loaning against it.

Sure, that makes sense. Truthfully, I always thought that money would be better invested straight on financial investments rather than funneling it through a life insurance coverage plan Until I uncovered how IBC might be incorporated with an Irrevocable Life Insurance Coverage Count On (ILIT) to produce generational wealth. Let's begin with the essentials.

Infinite Power Bank

When you obtain against your plan's money worth, there's no collection payment timetable, providing you the liberty to manage the funding on your terms. At the same time, the money value remains to expand based upon the plan's warranties and dividends. This setup permits you to access liquidity without interrupting the long-term growth of your plan, provided that the loan and interest are managed carefully.

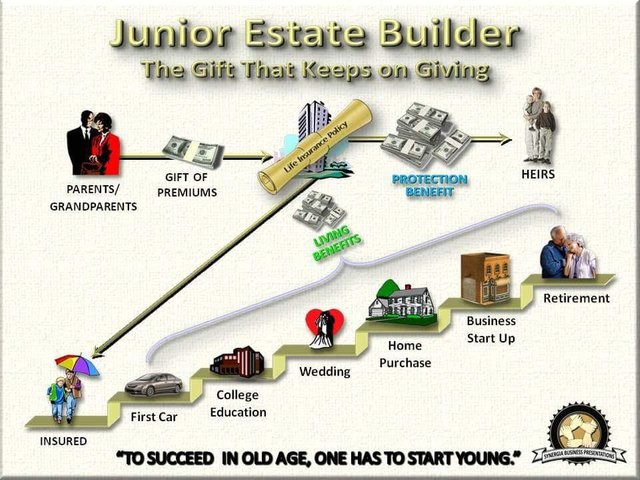

The procedure continues with future generations. As grandchildren are birthed and grow up, the ILIT can buy life insurance policy plans on their lives. The count on after that accumulates numerous plans, each with expanding money worths and death advantages. With these policies in area, the ILIT successfully ends up being a "Family members Bank." Relative can take lendings from the ILIT, making use of the cash money worth of the policies to fund financial investments, start businesses, or cover major costs.

A critical aspect of managing this Family Financial institution is the use of the HEMS standard, which stands for "Health, Education And Learning, Upkeep, or Assistance." This guideline is frequently included in trust fund agreements to guide the trustee on how they can distribute funds to beneficiaries. By sticking to the HEMS criterion, the trust fund guarantees that distributions are made for crucial needs and long-lasting assistance, safeguarding the trust's possessions while still attending to relative.

Raised Versatility: Unlike inflexible small business loan, you control the payment terms when borrowing from your own plan. This permits you to structure settlements in such a way that straightens with your company cash circulation. infinite banking nelson nash. Enhanced Money Circulation: By funding overhead with policy lendings, you can potentially maximize money that would or else be linked up in conventional loan settlements or devices leases

He has the same devices, but has actually also constructed added cash money value in his plan and obtained tax obligation advantages. Plus, he currently has $50,000 available in his policy to use for future opportunities or costs. Despite its possible benefits, some individuals continue to be skeptical of the Infinite Financial Concept. Let's resolve a few typical issues: "Isn't this just pricey life insurance policy?" While it holds true that the costs for a properly structured whole life policy may be higher than term insurance policy, it is necessary to watch it as more than just life insurance policy.

Be Your Own Banker Life Insurance

It's concerning developing an adaptable funding system that provides you control and supplies several advantages. When made use of strategically, it can match other investments and company methods. If you're captivated by the possibility of the Infinite Banking Idea for your organization, here are some actions to think about: Inform Yourself: Dive deeper right into the concept through respectable publications, workshops, or assessments with educated specialists.

{kind=link}

Table of Contents

Latest Posts

Byob: How To Be Your Own Bank

Banking Concept

Infinite Banking Calculator

More

Latest Posts

Byob: How To Be Your Own Bank

Banking Concept

Infinite Banking Calculator