All Categories

Featured

Table of Contents

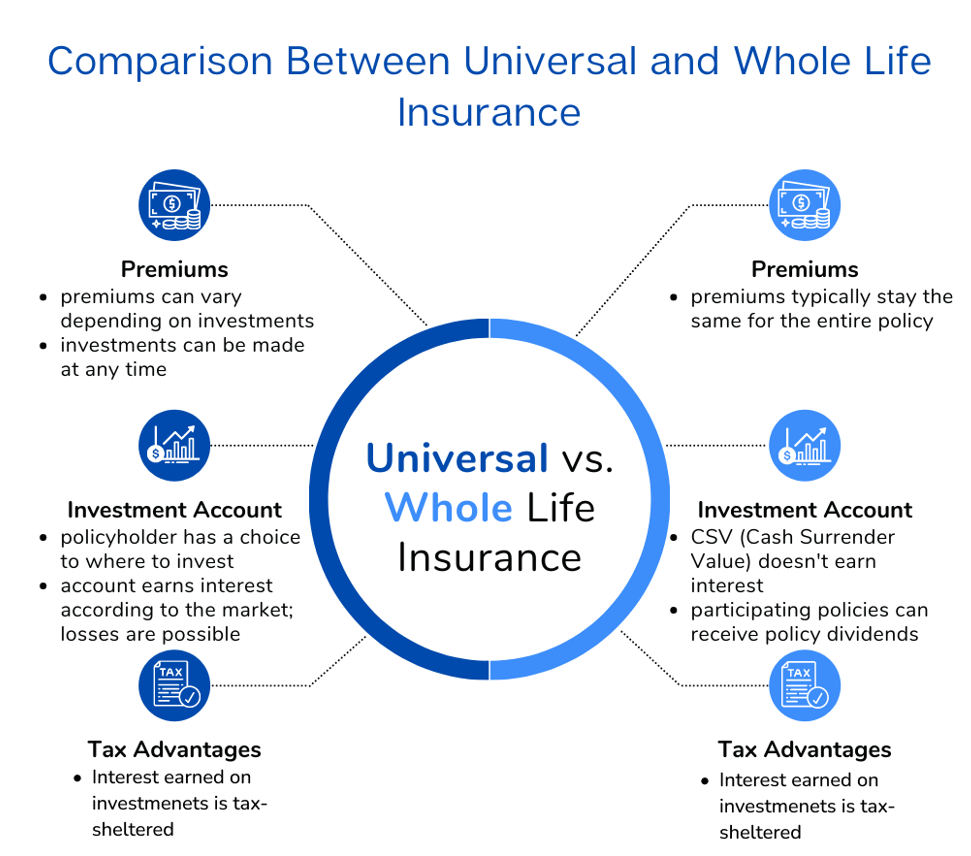

The are whole life insurance coverage and universal life insurance. The cash value is not added to the death advantage.

The policy loan passion rate is 6%. Going this course, the rate of interest he pays goes back right into his policy's cash worth rather of a monetary institution.

Infinite Banking Reviews

The principle of Infinite Financial was created by Nelson Nash in the 1980s. Nash was a money professional and fan of the Austrian school of business economics, which supports that the worth of products aren't clearly the result of conventional financial structures like supply and demand. Instead, individuals value cash and items in a different way based on their financial condition and demands.

One of the challenges of conventional banking, according to Nash, was high-interest prices on lendings. Way too many people, himself included, got right into financial problem due to reliance on banking institutions. Long as banks set the passion rates and lending terms, people really did not have control over their own wide range. Becoming your own banker, Nash determined, would certainly put you in control over your economic future.

Infinite Banking requires you to own your financial future. For goal-oriented individuals, it can be the very best economic tool ever before. Right here are the advantages of Infinite Banking: Perhaps the single most beneficial aspect of Infinite Banking is that it boosts your cash money circulation. You do not need to go through the hoops of a standard bank to get a finance; just demand a plan loan from your life insurance policy company and funds will certainly be provided to you.

Dividend-paying entire life insurance policy is very reduced risk and uses you, the policyholder, a wonderful deal of control. The control that Infinite Financial uses can best be grouped into 2 categories: tax obligation advantages and possession protections - a life infinite. Among the factors entire life insurance policy is excellent for Infinite Banking is just how it's tired.

Infinite Banking Concept Wiki

When you make use of whole life insurance policy for Infinite Financial, you participate in a private contract between you and your insurance provider. This privacy uses specific property securities not discovered in various other economic vehicles. These securities might differ from state to state, they can consist of protection from possession searches and seizures, security from judgements and protection from lenders.

Entire life insurance policy plans are non-correlated properties. This is why they work so well as the monetary structure of Infinite Financial. No matter of what occurs in the market (supply, real estate, or otherwise), your insurance coverage policy maintains its worth.

Market-based financial investments expand wealth much faster yet are exposed to market fluctuations, making them inherently high-risk. What happens if there were a 3rd bucket that offered safety and security but likewise modest, surefire returns? Entire life insurance policy is that third bucket. Not only is the rate of return on your entire life insurance policy policy ensured, your survivor benefit and premiums are additionally guaranteed.

This framework aligns flawlessly with the concepts of the Perpetual Wide Range Strategy. Infinite Banking interest those looking for higher financial control. Here are its main benefits: Liquidity and access: Policy lendings supply immediate access to funds without the restrictions of traditional small business loan. Tax obligation efficiency: The cash value grows tax-deferred, and plan loans are tax-free, making it a tax-efficient tool for constructing wealth.

Infinite Banking Book

Property defense: In many states, the money worth of life insurance coverage is protected from lenders, including an added layer of financial safety. While Infinite Financial has its merits, it isn't a one-size-fits-all remedy, and it includes substantial drawbacks. Below's why it may not be the finest approach: Infinite Financial typically needs detailed policy structuring, which can confuse insurance policy holders.

Visualize never ever having to fret regarding small business loan or high rates of interest once more. What if you could borrow cash on your terms and build wealth at the same time? That's the power of unlimited financial life insurance policy. By leveraging the cash money value of whole life insurance policy IUL plans, you can expand your wealth and borrow money without depending on conventional financial institutions.

There's no collection lending term, and you have the flexibility to choose on the payment routine, which can be as leisurely as settling the financing at the time of death. This flexibility encompasses the servicing of the lendings, where you can choose interest-only repayments, keeping the car loan equilibrium level and workable.

Holding money in an IUL fixed account being credited interest can typically be better than holding the money on down payment at a bank.: You've always desired for opening your very own bakeshop. You can borrow from your IUL plan to cover the first expenditures of renting out a space, buying devices, and employing staff.

Infinite Bank Statement

Individual finances can be obtained from traditional financial institutions and debt unions. Borrowing cash on a credit history card is usually really pricey with yearly portion rates of passion (APR) often getting to 20% to 30% or even more a year.

The tax therapy of plan financings can vary considerably depending upon your country of residence and the particular terms of your IUL plan. In some regions, such as North America, the United Arab Emirates, and Saudi Arabia, plan lendings are normally tax-free, offering a significant advantage. In other jurisdictions, there may be tax obligation ramifications to take into consideration, such as prospective tax obligations on the funding.

Term life insurance just gives a death benefit, without any money worth accumulation. This means there's no cash money value to borrow versus.

For car loan policemans, the comprehensive guidelines enforced by the CFPB can be seen as cumbersome and limiting. Finance officers commonly suggest that the CFPB's policies develop unnecessary red tape, leading to even more paperwork and slower finance processing. Guidelines like the TILA-RESPA Integrated Disclosure (TRID) policy and the Ability-to-Repay (ATR) demands, while intended at protecting customers, can result in hold-ups in shutting deals and boosted functional costs.

{kind=link}

Table of Contents

Latest Posts

Byob: How To Be Your Own Bank

Banking Concept

Infinite Banking Calculator

More

Latest Posts

Byob: How To Be Your Own Bank

Banking Concept

Infinite Banking Calculator